Finweek has reported that 78% of respondents in a recent survey claimed that their salaries did not cover their living costs when they were faced with an unexpected expense. Just 31% of respondents said they had a separate savings account for rainy days or an emergency. With food inflation at a six percent creep, and increasing fuel and utilities costs, consumers are turning to personal loans to cover the shortfall in their monthly finances.

Finweek has reported that 78% of respondents in a recent survey claimed that their salaries did not cover their living costs when they were faced with an unexpected expense. Just 31% of respondents said they had a separate savings account for rainy days or an emergency. With food inflation at a six percent creep, and increasing fuel and utilities costs, consumers are turning to personal loans to cover the shortfall in their monthly finances.

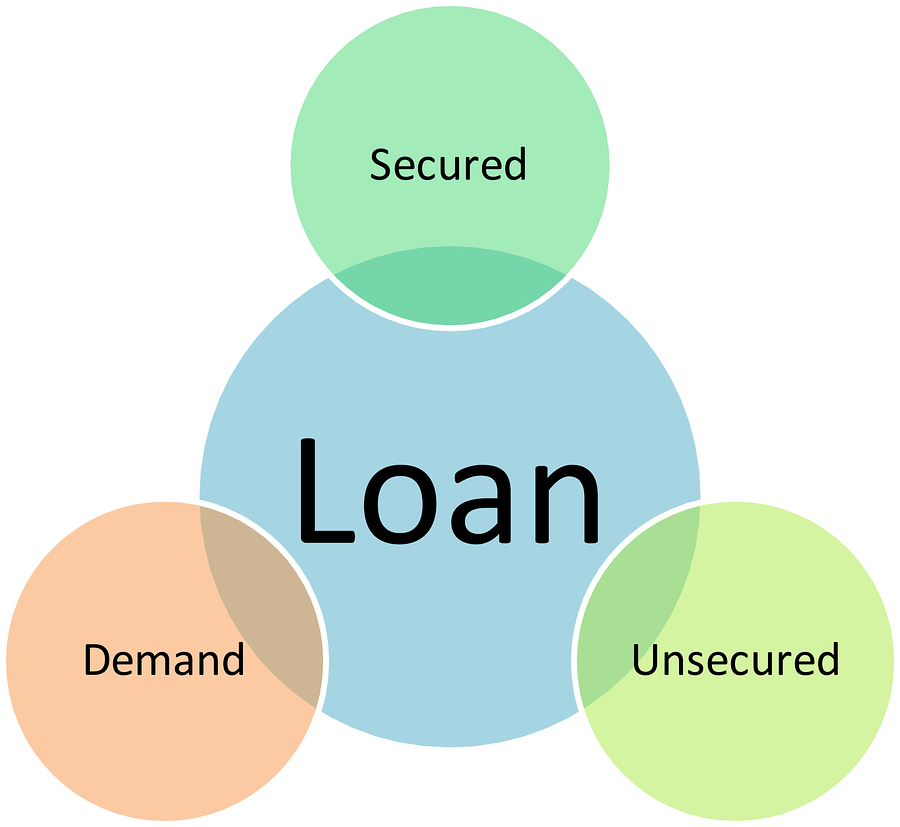

Understanding personal loans

A personal loan allows an individual to borrow money from a financial institution for personal use. The amount could be as large as a mortgage loan or a smaller sum to cover medical costs, car repairs, a broken appliance, home improvements or bill consolidation. The attraction of a personal loan is that an individual can make a purchase or pay an expense without having to save up the funds first.

Personal loans are repaid, along with interest, to the financial institution in the form of monthly payments over an agreed period of time which can be as short a month in the case of payday loans or twenty years when repaying a mortgage. The loan amount is either secured or unsecured.

Short term, unsecured loans

The rise in popularity of short term personal, or signature, loans is because they are for small sums of money, ranging from a few hundred rand to R8000 that can be repaid easily if borrowed wisely. Also, the borrower does not have to provide security for the loan, which is issued and supported only by the borrower's creditworthiness. Repayment terms for short term, unsecured personal loans are typically from 12 to 48 months. Since there is no asset for the lender to repossess if the borrower defaults on the loan, unsecured loans carry a higher interest rate than secured loans.

This type of loan, offered in South Africa by lenders like Wonga.co.za, is usually borrowed for up to a month. Although Wonga ZA loans are not secured by an asset, there can still be consequences in the form of penalties and fees if the loan is not repaid on time and to the agreed terms.

Despite higher interest rates, the loan can mean the difference between paying a one-off car repair or not being able to drive for months.

Long term, secured loans

A secured loan requires some type of collateral, and the loan amount is usually a percentage of the value of the collateral.

Secured loans tend to be for larger amounts of money and for longer periods of time, typically five years or more. Home loans are one type of secured loan: the amount of the loan is borrowed against the value of a property. But smaller secured loans exist, which are also tied into a borrower's personal assets.

Failure to repay a secured loan can result in the loss of a property or car as the lender attempts to recover the amount owed and interest on the loan. Secured loans usually provide the option of higher borrowing limits and lower interest rates and are generally easier to qualify for.

There is generally a choice of fixed or variable interest rates on secured loans. Fixed rates involve monthly payments that stay the same for the term of the loan. Variable interest rates may seem more attractive because the initial interest rate is usually lower than fixed rates, but a bank can adjust variable interest rate loans and if the interest rate rises, so does the monthly payment.

Deciding for or against a personal loan

A personal loan allows a borrower to instantly solve a short term financial problem or build long term financial security. It can provide fixed interest rates and repayments that can budgeted for, but important questions should always be asked before applying for a loan.

• Have you done your homework? Never make a financial commitment without researching available products on the market and alternative solutions to a temporary financial fix.

• Can you afford to repay the loan? If you have any doubts, don't take the loan in the first place.

• Have you taken into account that the total amount you have to repay may be higher because you're paying interest over a longer period? Always look at the full cost of a loan as well as the amount of individual repayments.

• What fees will you be paying? Some loan deals have additional fees and dues. Make sure these cost have been taken into account.

• Do you understand all the terms and conditions of your personal loan agreement? Do not allow yourself to be rushed or bamboozled with jargon. Read the fine print and ask for clarity from your personal loan provider.