People apply for a personal loan to start a new business, buy a car, plan weddings, basically, they use it as per their discretion. This kind of loan is readily available from numerous lenders and NBFCs that offer schemes with varying clauses.

Although it’s not too much of a trouble to get a personal loan nowadays, it’s important that you ask the following questions to yourself—loan is right for your need, or your lender—so that you don’t jeopardise your financial stability.

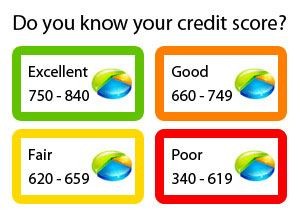

What is my Credit Score?

You loan qualification depends a lot on your credit score. Not just that, the interest rate will also be determined by the credit score you have.

The credit score is basically your financial track record that contains details of the loans you signed up for, credit card limits, and liabilities. If you have a low credit score, it is advisable that you improve it before applying for personal loan and repay it on time.

How Much Money do I Really Need?

When situations demand the need for immediate finance, personal loan is what people usually opt for. Before approaching the lender, make sure that you have a fair idea of how much money you need exactly.

You can create monthly cash-flow projections to understand your financial requirements. Calculate your expenses and assimilate them; then reserve a portion of your income for savings and EMIs. Figuring these out will give an idea if you can afford taking the loan.

What is the Loan Application Process?

The loan application process is the first step towards approaching your lender. As a part of the process you’ll have to submit your personal, professional, and financial documents to pass their eligibility to get your loan application approved.

What Do you Need to Get the Loan Approved?

In some cases, giving your credit score and income sheet is enough for getting a personal loan approved. However, in other cases, you might need to provide your tax returns and bank statements to prove how many assets you have and how much money you rake in every month.

What is my Interest Rate?

What is my Interest Rate?

The interest rate would be stated in terms of Annual Percentage Rate (APR) in most cases. It can be defined as the annual interest rate that is being charged for borrowing. Thus, you can use this to calculate the total amount you need to pay to the lender and how much you are being charged.

Can I Afford the EMI?

Use the personal loan calculator to calculate the EMI you would need to pay to your lender. Different banks might have different methods of interest rate computation and your EMI would depend on that even if the lenders charge the same interest rate.

What are the Added Costs?

Interest rate is not the only charge you pay to the lender when you avail of a personal loan. There is a processing fee as well which can either be fixed or a percentage of your entire loan amount. Besides this charge, there can be hidden clauses in the policy that can levy agent’s fee and additional taxes.

What is the Repayment Period?

This is the time you will get to repay the loan. All you have to remember here is that higher the EMI, lower is the interest charge and tenure. However if you decide to pay lower EMIs, the tenure and interest charges shoot up.

![An Explanation of Small Business Loans [Infographic]](https://lerablog.org/wp-content/plugins/wp-thumbie/timthumb.php?src=http://lerablog.org/wp-content/uploads/2017/05/grthrhe-300x200.jpg&w=300&h=140&zc=1)